2026年4月 何故アメリカのターゲット(TGT)の株が上昇しているのか?

長らく低調が続いていたアメリカの小売大手・ターゲット(NYSE: TGT)の株価が、2026年4月に入って急上昇しています。年初来では一時30%超の上昇を記録し、4月14日$301C21日のわずか1週間でも約10%上げました。何がこの反発を引き起こしたのか。その理由と今後の見通しを、信頼性の高い複数のニュースソースをもとに整理して解説します。

※出来るだけ正確なソースを利用していますが投資は自己判断でお願いします。

Contents

- 0.1 ざっくり要点(結論)

- 0.2 上昇の背景①:3月決算と新CEOの再建戦略

- 0.3 上昇の背景②:アナリストが相次いで強気に転換(4月15$301C21日)

- 0.4 上昇の背景③:関税還付の期待感(4月20日)

- 0.5 株価の動き(直近1週間)

- 0.6 今後の見通しとリスク・注意点

- 0.7 まとめ

- 1 April 2026: Why Is Target (TGT) Stock Rising?

- 1.1 The Short Answer

- 1.2 Driver 1: A Credible Turnaround Story $2014 Starting with Q4 Earnings

- 1.3 Driver 2: Wall Street Upgrades in Quick Succession (April 15$201321)

- 1.4 Driver 3: Tariff Refund Expectations (April 20)

- 1.5 Price Action: The Past Week at a Glance

- 1.6 Outlook: Bull Case vs. Risk Factors

- 1.7 Summary

ざっくり要点(結論)

ここ数日のTGT上昇は、"1本の大きなニュース"によるものではありません。

①アナリストによる強気な目標株価の引き上げ

②関税還付への期待

③3月決算を起点とした「ターンアラウンド(経営再建)期待」の継続的な買い直しという、3つの流れが重なった結果です。

| 要因 | 内容 | 時期 |

|---|---|---|

| アナリスト強気転換 | Guggenheim・Evercore・Morgan Stanleyなどが目標株価を相次ぎ引き上げ | 4月14$301C21日 |

| 関税還付の期待 | 輸入業者向け関税還付の可能性が報道され、コスト圧迫懸念が後退 | 4月20日 |

| 3月決算の好結果 | 新CEO初の決算でEPSが予想を大幅上回り、成長戦略も発表 | 3月初旬$301C継続 |

| 市場全体のリスクオン | 地政学リスク後退・金利低下が小売株全体を押し上げ | 4月上旬$301C |

上昇の背景①:3月決算と新CEOの再建戦略

今回の株価上昇を語るうえで欠かせないのが、3月初旬の決算発表です。新CEO・マイケル・フィデルケ氏のもとで発表された2025年度第4四半期(Q4)決算では、EPS(1株利益)が市場予想の$2.17に対して$2.44と大幅な上振れを記録。通期の売上見通しも市場予想を超え、株価はその日1日で7%急騰しました。

さらに注目されたのが成長戦略の中身です。フィデルケCEOは、店舗改装・新規出店・買い物体験の改善・配送インフラ強化に20億ドル超を投資する方針を明らかにし、2月の売上が改善傾向にあることも強調。「2024$301C2025年の低迷から抜け出す」という再建ストーリーが市場に信頼感を与え、以降の買いの土台となりました。

上昇の背景②:アナリストが相次いで強気に転換(4月15$301C21日)

4月に入ってからの上昇を直接的に後押ししたのが、複数の大手証券会社によるレーティング・目標株価の引き上げです。

- Morgan Stanley:目標株価$145・Overweight(強気)維持。店舗運営の改善、商品構成の刷新、来店客数の回復を根拠に「ターンアラウンドが見えてきた」とコメント。

- Guggenheim:4月20日に目標株価を$130から$140に引き上げ。「売上モメンタムの転換点が来た」と評価し「買い」継続。

- Evercore ISI:4月21日に目標株価を$120から$125に引き上げ。

- DA Davidson:目標株価$140で「買い」を維持。

同期間、Goldman Sachsも実店舗の現場調査をもとに「ベビー用品売り場や自社ブランド『Threshold』コーナーの改装が確認でき、今後も四半期ごとに売り場の"新しさ"が増す」と報告。実際の店舗変化が数字で確認され始めたことが、アナリストの相次ぐ強気転換につながりました。

上昇の背景③:関税還付の期待感(4月20日)

4月20日、CNBCが「WalmartとTargetが関税の数十億ドル規模の還付を受け取れる可能性がある」と報道しました。ターゲットは輸入品への依存度が高く、関税コストが業績を圧迫するリスクとして長らく懸念されてきました。この報道はそうした懸念を和らげる材料として受け止められ、買いをさらに後押ししました。

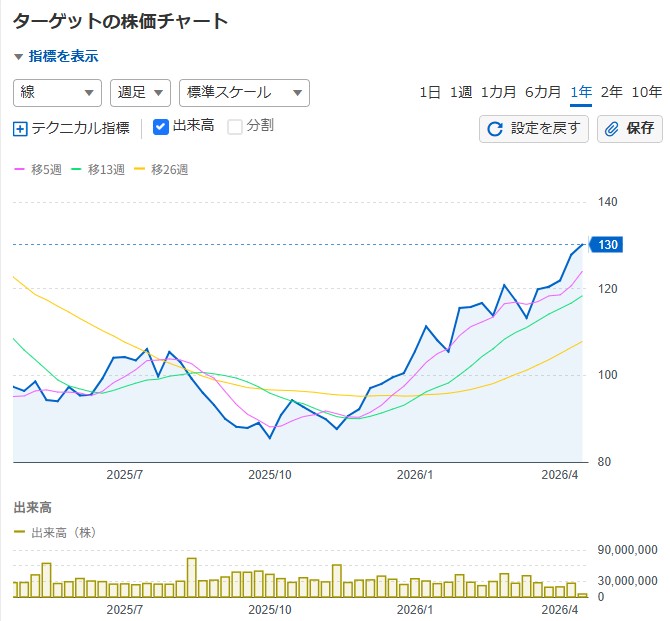

株価の動き(直近1週間)

| 日付 | 株価 | 前日比 | 主な出来事 |

|---|---|---|---|

| 4月14日(月) | $119.53 | $2014 | 週初 |

| 4月15日(火) | +2.62% | ↑ | CNBCがS&P500アウトパフォームを報道。アナリスト強気報告 |

| 4月17日(木) | $127.84 | +3.01% | GurFocusがモメンタムランク10/10と評価 |

| 4月20日(日) | +1.82% | ↑ | Guggenheim目標株価引き上げ、関税還付報道 |

| 4月21日(月) | $132.10$301C$133.10 | +1.34% | Evercore ISI目標株価引き上げ、52週高値更新 |

4月14日から21日のわずか1週間で約10%強の上昇。年初来では一時+30%超を記録しています(52週安値$83.44からの回復)。

今後の見通しとリスク・注意点

強気派の見方(メリット)

- 新CEOのもとで店舗改装・デジタル強化・AI活用など具体的な施策が進行中

- EPS(利益)は改善傾向にあり、コスト管理が機能し始めている

- 配当利回り約3.5$301C4%と高く、インカム投資家にも魅力

- Target Circle(会員サービス)やRoundel(広告事業)など収益性の高い新事業が成長中

- 関税還付が実現すれば、さらなる利益改善につながる可能性

慎重派の見方(リスク)

- 売上はまだ弱く、2025年度通期で前年比$22122%。本格的な客数回復はこれから

- アナリストの平均目標株価(約$116$301C$119)は直近株価($130超)をすでに下回っている。期待が先行気味

- Bank of Americaなど一部は「アンダーパフォーム」評価を継続

- 関税問題・消費者信頼感の悪化など外部リスクは依然として存在

- 5月下旬予定のQ1決算で、実際の業績回復が確認されなければ調整リスクあり

注目すべき次のイベント:2026年5月下旬(5月20日予定)の第1四半期決算発表。ここで実際の売上・利益・来店客数の改善が数字で確認できるかどうかが、上昇トレンドの継続を左右します。

まとめ

- TGTは4月14$301C21日の1週間で約10%上昇、年初来では一時+30%超

- 直接のトリガーは「アナリストの目標株価引き上げ(Guggenheim・Evercore・Morgan Stanleyなど)」と「関税還付報道(4/20)」

- その土台には3月決算のEPS上振れと新CEOの成長戦略への期待がある

- 株価はモメンタム10/10と非常に強い短期勢いを示している

- 一方で、売上の本格回復はまだ途上。平均アナリスト目標株価は現在値を下回っており、期待先行の面も

- 次の判断材料は5月下旬のQ1決算。実績が伴うかどうかを要確認

April 2026: Why Is Target (TGT) Stock Rising?

After years of underperformance, shares of U.S. retail giant Target Corporation (NYSE: TGT) have surged sharply in April 2026 $2014 rising more than 10% in just one week (April 14$201321) and posting gains of over 30% year-to-date at their peak. Here’s what’s driving the move, and what to watch next.

※ This article is for informational purposes only and is not investment advice. Please make all investment decisions at your own discretion.

The Short Answer

TGT’s recent rally is not the result of a single catalyst. It reflects the convergence of three forces: (1) bullish analyst upgrades, (2) expectations of tariff refunds, and (3) a sustained re-rating of the stock as a genuine turnaround play, anchored by a strong Q4 earnings report in March.

| Driver | Detail | When |

|---|---|---|

| Analyst upgrades | Guggenheim, Evercore ISI, Morgan Stanley raised price targets | Apr 14$201321 |

| Tariff refund hopes | Reports that major retailers may recoup billions in import tariffs | Apr 20 |

| Q4 earnings beat | New CEO’s first report showed EPS well above estimates; new growth plan unveiled | Early March (ongoing) |

| Broader risk-on tone | Easing geopolitical risk and falling rates lifted retail stocks broadly | Early April onward |

Driver 1: A Credible Turnaround Story $2014 Starting with Q4 Earnings

The foundation of this rally was laid in early March. In his first earnings report as CEO, Michael Fiddelke delivered results that genuinely surprised the market: EPS of $2.44 vs. the consensus estimate of $2.17, along with a full-year sales outlook that also beat expectations. Shares jumped 7% on the day of the report.

Beyond the numbers, Fiddelke announced a strategic plan committing over $2 billion to store remodels, new locations, supply chain modernization, and digital investments. He also noted that sales trends had improved in February, giving investors confidence that the multi-year slump $2014 during which the stock fell more than 50% from its 2021 peak $2014 may finally be reversing.

Driver 2: Wall Street Upgrades in Quick Succession (April 15$201321)

What transformed the Q4 optimism into an April rally was a string of analyst upgrades that gave the move fresh momentum:

- Morgan Stanley $2014 PT $145, Overweight. Called the turnaround “increasingly visible" citing store operations, merchandise improvements, and traffic recovery.

- Guggenheim (Apr 20) $2014 Raised PT from $130 to $140. Cited a “top-line inflection point" and maintained its Buy rating.

- Evercore ISI (Apr 21) $2014 Raised PT from $120 to $125.

- DA Davidson $2014 Maintained PT of $140 with a Buy rating.

Goldman Sachs also contributed with a store-check report that confirmed physical improvements $2014 remodeled baby aisles, expanded Threshold private-label sections $2014 supporting the thesis that Target’s in-store experience is genuinely improving on a quarter-by-quarter basis.

Driver 3: Tariff Refund Expectations (April 20)

On April 20, CNBC reported that major U.S. retailers including Walmart and Target could be in line to receive billions of dollars in tariff refunds under a potential policy change. Given that Target sources a significant portion of its inventory from tariff-affected regions, this news meaningfully reduced a key risk that had been weighing on the stock.

Price Action: The Past Week at a Glance

| Date | Price / Move | Key Event |

|---|---|---|

| Apr 14 (Mon) | $119.53 | Week open |

| Apr 15 (Tue) | +2.62% | CNBC notes TGT outperforming S&P 500; multiple analyst notes |

| Apr 17 (Thu) | $127.84 / +3.01% | Momentum rank 10/10 flagged by GuruFocus |

| Apr 20 (Sun) | +1.82% | Guggenheim upgrade; tariff refund report |

| Apr 21 (Mon) | $132.10$2013$133.10 / +1.34% | Evercore ISI upgrade; 52-week high set |

Over this single week, TGT gained roughly 10%+, and year-to-date the stock had climbed more than 30% from its 52-week low of $83.44.

Outlook: Bull Case vs. Risk Factors

Bull Case

- Concrete execution underway: store remodels, AI investment, stronger digital sales (now 20%+ of total)

- Earnings quality improving even as top-line recovery continues $2014 EPS beat in Q4 is a meaningful signal

- Dividend yield of ~3.5$20134% offers income cushion; Target is a “Dividend King" with decades of consecutive increases

- High-margin new businesses (Target Circle 360 membership, Roundel ad platform) growing rapidly

- Tariff refunds, if confirmed, would provide a direct profit boost

Risk Factors to Watch

- Top-line growth remains elusive $2014 full-year fiscal 2025 revenue fell ~2% YoY

- The average analyst price target (~$116$2013$119) is now below the current share price, suggesting expectations may be stretched

- Bank of America and others maintain Underperform ratings

- Consumer confidence remains fragile; tariff and inflation risks are not fully resolved

- Q1 2026 earnings (expected ~May 20) will be the real test $2014 if the sales recovery doesn’t show up in the numbers, a pullback is likely

The next major catalyst: Q1 FY2026 earnings, expected around May 20, 2026. This report will show whether improving traffic, better merchandise, and margin recovery are actually translating into sustained financial results.

Summary

- TGT rose ~10% in the week of April 14$201321, and is up 30%+ YTD from its 52-week low

- The immediate triggers were analyst price target increases (Guggenheim, Evercore ISI, Morgan Stanley) and tariff refund expectations (Apr 20)

- The underlying driver is renewed confidence in the CEO Fiddelke’s turnaround plan, anchored by a Q4 EPS beat and a credible multi-billion dollar investment strategy

- Momentum indicators are at maximum strength (10/10), but the average analyst PT is now below the stock price $2014 signaling some caution

- The real verdict comes in May: Q1 earnings will confirm or challenge the turnaround narrative

FX初心者には必須 無料のうちにGET!